5. Linear Optimization and the Simplex Method#

5.1. Linear Optimization#

TODO: Write this section better and in more detail

I’m assuming LP is explained in the lectures already but here is a short reminder.

We want to solve problems that are of the form

where \(x\in\reals^n\) are the decision variables, \(A\in\reals^{m\times n}\) and \(b\in\reals^m\) specify the constraints, and \(c\in\reals^n\) gives the linear objective. LPs of other forms can be transformed into this form as well. In the lectures, you probably learnt that an LP has a (bounded) optimal solution, then there exists an extreme point of the feasible region which is optimal.

Since at least one vertex is guaranteed to be the optimum, one can just go through every edge to find it. The simplex algorithm does so, in an efficient way (most of the time).

5.2. The Simplex Method#

In order to describe the basic simplex algorithm, consider an objective function of the form

If we know that all \(x_i\geq 0\), then we can maximize it by setting all variables to \(0\), giving us the optimal value as \(a\). Thus the problem of optimizing (5.1) becomes a problem of rewriting it in the form of (5.2).

To exemplify this, consider the following LP

The first step is to rewrite (5.3) in the canonical form, where

inequality constraints are converted to equality constraints by adding non-negative slack variables,

all variables are non-negative

the constraints are written so that the slack variables are left on one side.

In the above, the set of (lone) variables in the LHS of the constraints (also called basic variables) correspond to the vertices of the polyhedral that is the feasible region. By substituting the nonbasic variables in the LP with the basic ones, one is in effect iterating through the vertices of the feasible region, which will ultimately yield the optimal solution.

Actually doing so involves making decisions, for example which variable in the objective function to replace, and which constraint to rewrite it with. For the purposes of this example, we’ll first choose \(x_1\), and rewrite it using the most limiting constraint, which we obtain by posing the question “What is the largest value \(x_1\) can have among the constraints?”

\(x_3=7-2x_1-x_2\) |

\(x_1\leq 3.5\) |

\(x_4=4-x_1-x_2 \) |

\(x_1\leq 4\) |

\(x_5=9-x_1-3x_2\) |

\(x_1\leq 9\) |

We can see that the most limiting constraint is \(x_3=7-2x_1-x_2\), so we solve for \(x_1\) to get \(x_1=3.5-0.5x_2-0.5x_3\). Substituting this to all \(x_1\)s yields

This completes a single iteration of the algorithm. By repeating until no positive variable is left in the objective function, one obtains the entire algorithm.

5.3. Visualization#

The visualization below is obtained via GILP.

Important

These visualizations working require require.js as noted here.

However, the way to include them there puts this in every page, which is not necessary and potentially conflicting with other js frameworks (I couldn’t get d3 to work in Gradient-based optimization).

So make sure you add something like

```{raw} html

<script src="https://cdnjs.cloudflare.com/ajax/libs/require.js/2.3.4/require.min.js"></script>

```

at the start of your page when using this.

You can hover over the vertices to see additional information, such as the value of the objective function at that point (labeled Obj), or the basic variables associated with the vertex (labeled B).

import numpy as np

from gilp.simplex import LP

from gilp.visualize import simplex_visual

A = np.array([[2,1],

[1,1],

[1,3]])

b = np.array([7,4,9])

c = np.array([40, 60])

lp = LP(A,b,c)

simplex_visual(lp).show(renderer="notebook")

5.4. More involved example#

5.4.1. Problem#

Taken from [Wil13] Chapter 12.1.

A food is manufactured by refining raw oils and blending them together. The raw oils are of two categories:

Vegetable oils |

VEG 1 |

VEG 2 |

|

Non-vegetable oils |

OIL 1 |

OIL 2 |

|

OIL 3 |

Each oil may be purchased for immediate delivery (January) or bought on the futures market for delivery in a subsequent month. Prices at present and in the futures market are given below in (£/ton):

VEG 1 |

VEG 2 |

OIL 1 |

OIL 2 |

OIL 3 |

|

|---|---|---|---|---|---|

January |

110 |

120 |

130 |

110 |

115 |

February |

130 |

130 |

110 |

90 |

115 |

March |

110 |

140 |

130 |

100 |

95 |

April |

120 |

110 |

120 |

120 |

125 |

May |

100 |

120 |

150 |

110 |

105 |

June |

90 |

100 |

140 |

80 |

95 |

The final product sells at £150 per ton.

Vegetable oils and non-vegetable oils require different production lines for refining. In any month, it is not possible to refine more than 200 tons of vegetable oils and more than 250 tons of non-vegetable oils. There is no loss of weight in the refining process, and the cost of refining may be ignored.

It is possible to store up to 1000 tons of each raw oil for use later. The cost of storage for vegetable and non-vegetable oil is £5 per ton per month. The final product cannot be stored, nor can refined oils be stored.

There is a technological restriction of hardness on the final product. In the units in which hardness is measured, this must lie between 3 and 6. It is assumed that hardness blends linearly and that the hardnesses of the raw oils are

VEG |

8.8 |

VEG 2 |

6.1 |

OIL 1 |

2.0 |

OIL 2 |

4.2 |

OIL 3 |

5.0 |

What buying and manufacturing policy should the company pursue in order to maximise profit?

At present, there are 500 tons of each type of raw oil in storage. It is required that these stocks will also exist at the end of June.

5.4.2. Modeling#

The problem presented here has two aspects. Firstly, it is a series of simple blending problems. Secondly, there is a purchasing and storing problem. To understand how this problem may be formulated, it is convenient to consider first the blending problem for only one month.

5.4.2.1. The single-period problem#

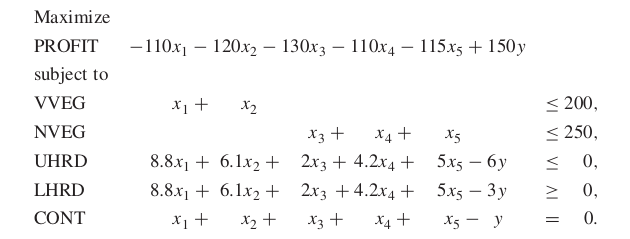

If no storage of raw oils were allowed, the problem of what to buy and how to blend in January could be formulated as follows:

The variables x 1 , x 2 , x 3 , x 4 , x 5 represent the quantities of the raw oils that should be bought respectively, that is, VEG 1, VEG 2, OIL 1, OIL 2 and OIL 3. y represents the quantity of PROD that should be made.

The objective is to maximize profit, which represents the income derived from selling PROD minus the cost of the raw oils.

The first two constraints represent the limited production capacities for refin- ing vegetable and non-vegetable oils.

The next two constraints force the hardness of PROD to lie between its upper limit of 6 and its lower limit of 3. It is important to model these restrictions correctly. A frequent mistake is to model them as

and

Such constraints are clearly dimensionally wrong. The expressions on the left have the dimension of hardness multiplied by quantity, whereas the figures on the right have the dimensions of hardness. Instead of the variables x i in the above two inequalities, expressions x i /y are needed to represent proportions of the ingredients rather than the absolute quantities x i . When such replacements are made, the resultant inequalities can easily be re-expressed in a linear form as the constraints UHRD and LHRD.

Finally, it is necessary to make sure that the weight of the final product PROD is equal to the weight of the ingredients. This is done by the last constraint CONT, which imposes this continuity of weight.

The single-period problems for the other months would be similar to that for January apart from the objective coefficients representing the raw oil costs.

5.4.2.2. The multi-period problem#

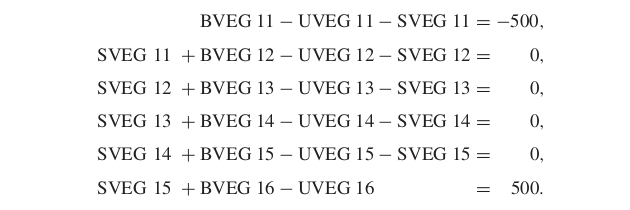

The decisions of how much to buy each month with a view to storing for use later can be incorporated into a linear programming model. To do this, a ‘multi- period’ model is built. It is necessary, each month, to distinguish the quantities of each raw oil bought, used and stored. These quantities must be represented by different variables. We suppose the quantities of VEG 1 bought, used and stored in each successive month are represented by variables with the following names:

BVEG 11, |

BVEG 12, |

and so on, |

UVEG 11, |

UVEG 12, |

Und so on, |

SVEG 11, |

SVEG 12, |

and so on. |

It is necessary to link these variables together by the relation

Initially (month 0) and finally (month 6), the quantities in store are constants

(500). The relation above involving VEG 1 gives rise to the following constraints:

Similar constraints must be specified for the other four raw oils.

It may be more convenient to introduce variables SVEG 10, and so on, and SVEG 16, and so on, into the model and fix them at the value 500.

In the objective function, the ‘buying’ variables will be given the appropriate raw oil costs in each month. The storage variables will be given the cost of £5 (or ‘profit’ of –£5). Separate variables PROD 1, PROD 2, and so on, must be defined to represent the quantity of PROD to be made in each month. These variables will each have a profit of £150.

The resulting model will have the following dimensions as well as the single objective function:

\(6\times 5=30\) |

buying variables |

\(6\times 5=30\) |

using variables |

\(6\times 5=30\) |

storing variables |

6 |

product variables |

Total 91 |

variables |

\(6\times 5=30\) |

blending constraints |

\(6\times 5=30\) |

storage linking constraints |

Total 60 |

constraints |

It is also important to realize the use to which a model such as this might be put for medium-term planning. By solving the model in January, buying and blending plans could be determined for January together with provisional plans for the succeeding months. In February, the model would probably be resolved with revised figures to give firm plans for February together with provisional plans for succeeding months up to and including July. By this means, the best use is made of the information for succeeding months to derive an operating policy for the current month.

5.4.3. Solving#

I’m solving this in Python because the visualisations above are in Python. We can separate the pages and adapt if desired.

I must have entered something wrong because the profit doesn’t match what is given in the book. I blame not using a nice modeling language. For the final version of an example like this, it is probably better to use JuMP or a modeling framework in Python. The question is which (probably JuMP, since we can’t have both as executable). Also, if JuMP, then how often would we use GILP visualisations? Since we can’t have two languages in one file.

import numpy as np

import pandas as pd

from scipy.optimize import linprog

# in (month x oil) shape

oil_costs = np.array([[110, 120, 130, 110, 115],

[130, 130, 110, 90, 115],

[110, 140, 130, 100, 95],

[120, 110, 120, 120, 125],

[100, 120, 150, 110, 105],

[ 90, 100, 140, 80, 135]])

# let x be of the form (buying_vars, using_vars, storing_vars, product_vars)

# where x_vars is ordered (month1_oil1, month1_oil2, ..., month2_oil1, ...)

# and len(x)=91

# linprog minimizes, so c@x should be negative profits

c = -np.concatenate((-oil_costs.flatten(), # cost of buying

np.zeros(30), # using variables doesn't affect objective

np.full(25, -5), # cost of storing

np.full(6, 150))) # profit

## Equality constraints

A_storage = np.zeros((30, 91))

b_storage = np.array((-500,0,0,0,0,500)*5)

for oil in range(5):

# do january

A_storage[oil*6, (oil, 30+oil, 60+oil)] = (1,-1,-1)

for month in range(1, 5): # do middle months

A_storage[oil*6+month, (60+(month-1)*5+oil, month*5+oil, 30+month*5+oil, 60+month*5+oil)] = (1, 1,-1,-1)

# do june

A_storage[oil*6+5, (60+(5-1)*5+oil, 5*5+oil, 30+5*5+oil)] = (1, 1,-1)

A_continuity = np.zeros((6, 91))

b_continuity = np.zeros(6)

for month in range(6):

A_continuity[month, 30+month*5:30+(month+1)*5] = 1

A_continuity[month, 85+month] = -1

A_eq = np.vstack((A_storage, A_continuity))

b_eq = np.concatenate((b_storage, b_continuity))

## Inequality constraints (should be upper bounds)

A_production = np.zeros((12,91))

b_production = np.array((200, 250)*6)

A_hardness = np.zeros((12,91))

b_hardness = np.zeros(12)

for month in range(6):

A_production[month*2, 30+month*5:30+month*5+2] = 1 # for vegetable oils

A_production[month*2+1, 30+month*5+2:30+(month+1)*5] = 1 # for non-vegetable oils

A_hardness[month*2, 30+month*5:30+(month+1)*5] = (8.8, 6.1, 2, 4.2, 5) # upper limit

A_hardness[month*2+1, 30+month*5:30+(month+1)*5] = (-8.8, -6.1, -2, -4.2, -5) # lower limit (expressed as an upper bound)

A_hardness[month*2:(month+1)*2, 85+month] = (-6, 3)

A_ub = np.vstack((A_production, A_hardness))

b_ub = np.concatenate((b_production, b_hardness))

# variable bounds

## only storing variables have a bound of 1000, the rest is controlled by constraints

bounds = [(0,None)]*60 + [(0,1000)]*25 + [(0,None)]*6

res = linprog(c, A_ub, b_ub, A_eq, b_eq, bounds)

print(f"Profit=${-np.round(res.fun)}")

Profit=$120343.0

Purchase Plan

rows = ['Jan', 'Feb', 'Mar', 'Apr', 'May', 'Jun']

columns = ['VEG1', 'VEG2', 'OIL1', 'OIL2', 'OIL3']

purchase_plan = pd.DataFrame(columns=columns, index=rows, data=0.0)

for month in range(6):

for oil in range(5):

purchase_plan.iloc[month, oil] = np.round(res.x[month*5+oil],1)

purchase_plan

| VEG1 | VEG2 | OIL1 | OIL2 | OIL3 | |

|---|---|---|---|---|---|

| Jan | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Feb | 0.0 | 0.0 | 0.0 | 750.0 | 0.0 |

| Mar | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Apr | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| May | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Jun | 659.3 | 540.7 | 0.0 | 750.0 | 0.0 |

Monthly Consumption

monthly_consumption = pd.DataFrame(columns=columns, index=rows, data=0.0)

for month in range(6):

for oil in range(5):

monthly_consumption.iloc[month, oil] = np.round(res.x[30+month*5+oil],1)

monthly_consumption

| VEG1 | VEG2 | OIL1 | OIL2 | OIL3 | |

|---|---|---|---|---|---|

| Jan | 159.3 | 40.7 | 0.0 | 250.0 | 0.0 |

| Feb | 0.0 | 200.0 | 0.0 | 250.0 | 0.0 |

| Mar | 159.3 | 40.7 | 0.0 | 250.0 | 0.0 |

| Apr | 159.3 | 40.7 | -0.0 | 250.0 | -0.0 |

| May | 22.2 | 177.8 | 0.0 | 250.0 | 0.0 |

| Jun | 159.3 | 40.7 | 0.0 | 250.0 | 0.0 |

Inventory Plan

inventory_plan = pd.DataFrame(columns=columns, index=rows[:-1], data=0.0)

for month in range(5):

for oil in range(5):

inventory_plan.iloc[month, oil] = np.round(res.x[60+month*5+oil],1)

inventory_plan

| VEG1 | VEG2 | OIL1 | OIL2 | OIL3 | |

|---|---|---|---|---|---|

| Jan | 340.7 | 459.3 | 500.0 | 250.0 | 500.0 |

| Feb | 340.7 | 259.3 | 500.0 | 750.0 | 500.0 |

| Mar | 181.5 | 218.5 | 500.0 | 500.0 | 500.0 |

| Apr | 22.2 | 177.8 | 500.0 | 250.0 | 500.0 |

| May | 0.0 | -0.0 | 500.0 | 0.0 | 500.0 |

5.4.4. Solving with OR-Tools#

This solution seems to be correct.

from ortools.linear_solver import pywraplp

solver = pywraplp.Solver.CreateSolver("GLOP")

if not solver:

raise Exception("Couldn't create solver")

hardness = [8.8, 6.1, 2, 4.2, 5]

buying = [[solver.NumVar(0, solver.infinity(), f"B-{month}-{oil}") for oil in columns] for month in rows]

using = [[solver.NumVar(0, solver.infinity(), f"U-{month}-{oil}") for oil in columns] for month in rows]

storing = [[solver.NumVar(0, 1000, f"S-{month}-{oil}") for oil in columns] for month in rows[:-1]]

product = [solver.NumVar(0, solver.infinity(), f"P-{oil}") for month in rows]

print("Number of variables =", solver.NumVariables())

# storage constraints

for oil in range(5):

# do january

solver.Add(buying[0][oil] - using[0][oil] - storing[0][oil] == -500)

for month in range(1, 5): # do middle months

solver.Add(storing[month-1][oil] + buying[month][oil] - using[month][oil] == storing[month][oil])

# do june

solver.Add(storing[4][oil] + buying[5][oil] - using[5][oil] == 500)

for month in range(6):

solver.Add(sum(using[month]) == product[month]) # continuity

solver.Add(sum(using[month][:2]) <= 200)

solver.Add(sum(using[month][2:]) <= 250)

solver.Add(sum(hardness[oil]*using[month][oil] for oil in range(5)) <= 6*product[month])

solver.Add(sum(hardness[oil]*using[month][oil] for oil in range(5)) >= 3*product[month])

print("Number of constraints =", solver.NumConstraints())

cost_of_purchase = sum(oil_costs[month][oil]*buying[month][oil] for oil in range(5) for month in range(6))

cost_of_storage = 5*sum(sum(x) for x in storing)

revenue = 150*sum(product)

solver.Maximize(revenue - cost_of_purchase - cost_of_storage)

Number of variables = 91

Number of constraints = 60

def p(x, m=6):

for month in range(m):

for oil in range(5):

print(f"{x[month][oil]} = {x[month][oil].solution_value()}")

status = solver.Solve()

if status == pywraplp.Solver.OPTIMAL:

print("Solution:")

print(f"Objective value = {solver.Objective().Value():0.1f}")

p(buying)

p(using)

p(storing, 5)

for month in range(6):

print(f"{product[month]} = {product[month].solution_value()}")

print(solver)

else:

print("The problem does not have an optimal solution.")

Solution:

Objective value = 120342.6

B-Jan-VEG1 = 0.0

B-Jan-VEG2 = 0.0

B-Jan-OIL1 = 0.0

B-Jan-OIL2 = 0.0

B-Jan-OIL3 = 0.0

B-Feb-VEG1 = 0.0

B-Feb-VEG2 = 0.0

B-Feb-OIL1 = 0.0

B-Feb-OIL2 = 0.0

B-Feb-OIL3 = 0.0

B-Mar-VEG1 = 0.0

B-Mar-VEG2 = 0.0

B-Mar-OIL1 = 0.0

B-Mar-OIL2 = 0.0

B-Mar-OIL3 = 0.0

B-Apr-VEG1 = 0.0

B-Apr-VEG2 = 0.0

B-Apr-OIL1 = 0.0

B-Apr-OIL2 = 0.0

B-Apr-OIL3 = 0.0

B-May-VEG1 = 0.0

B-May-VEG2 = 0.0

B-May-OIL1 = 0.0

B-May-OIL2 = 0.0

B-May-OIL3 = 750.0

B-Jun-VEG1 = 659.2592592592594

B-Jun-VEG2 = 540.7407407407405

B-Jun-OIL1 = 0.0

B-Jun-OIL2 = 750.0

B-Jun-OIL3 = 0.0

U-Jan-VEG1 = 85.18518518518448

U-Jan-VEG2 = 114.8148148148155

U-Jan-OIL1 = 0.0

U-Jan-OIL2 = 250.00000000000003

U-Jan-OIL3 = 0.0

U-Feb-VEG1 = 85.18518518518539

U-Feb-VEG2 = 114.8148148148146

U-Feb-OIL1 = 0.0

U-Feb-OIL2 = 0.0

U-Feb-OIL3 = 250.0

U-Mar-VEG1 = 85.18518518518539

U-Mar-VEG2 = 114.8148148148146

U-Mar-OIL1 = 0.0

U-Mar-OIL2 = 0.0

U-Mar-OIL3 = 250.0

U-Apr-VEG1 = 159.25925925925938

U-Apr-VEG2 = 40.740740740740605

U-Apr-OIL1 = 0.0

U-Apr-OIL2 = 250.00000000000003

U-Apr-OIL3 = 0.0

U-May-VEG1 = 85.18518518518539

U-May-VEG2 = 114.8148148148146

U-May-OIL1 = 0.0

U-May-OIL2 = 0.0

U-May-OIL3 = 250.0

U-Jun-VEG1 = 159.25925925925938

U-Jun-VEG2 = 40.740740740740605

U-Jun-OIL1 = 0.0

U-Jun-OIL2 = 250.00000000000003

U-Jun-OIL3 = 0.0

S-Jan-VEG1 = 414.8148148148155

S-Jan-VEG2 = 385.1851851851845

S-Jan-OIL1 = 500.0

S-Jan-OIL2 = 249.99999999999997

S-Jan-OIL3 = 500.0

S-Feb-VEG1 = 329.62962962963013

S-Feb-VEG2 = 270.37037037036987

S-Feb-OIL1 = 500.0

S-Feb-OIL2 = 250.00000000000003

S-Feb-OIL3 = 250.0

S-Mar-VEG1 = 244.44444444444477

S-Mar-VEG2 = 155.5555555555553

S-Mar-OIL1 = 500.0

S-Mar-OIL2 = 250.00000000000003

S-Mar-OIL3 = 0.0

S-Apr-VEG1 = 85.18518518518539

S-Apr-VEG2 = 114.81481481481468

S-Apr-OIL1 = 500.0

S-Apr-OIL2 = 0.0

S-Apr-OIL3 = 0.0

S-May-VEG1 = 0.0

S-May-VEG2 = 7.665616012258528e-14

S-May-OIL1 = 500.0

S-May-OIL2 = 0.0

S-May-OIL3 = 500.0

P-4 = 450.00000000000006

P-4 = 450.00000000000006

P-4 = 450.00000000000006

P-4 = 450.00000000000006

P-4 = 450.00000000000006

P-4 = 450.00000000000006

<ortools.linear_solver.pywraplp.Solver; proxy of <Swig Object of type 'operations_research::MPSolver *' at 0x7f53ddf77570> >

import pandas as pd

from ortools.linear_solver import pywraplp

# Define input data

prices = pd.DataFrame(

index=["January", "February", "March", "April", "May", "June"],

data={

"VEG 1": [110, 130, 110, 120, 100, 90],

"VEG 2": [120, 130, 140, 110, 120, 100],

"OIL 1": [130, 110, 130, 120, 150, 140],

"OIL 2": [110, 90, 100, 120, 110, 80],

"OIL 3": [115, 115, 95, 125, 105, 135],

},

)

hardness = [8.8, 6.1, 2.0, 4.2, 5.0]

price_per_ton = 150

storage_cost_per_ton_per_month = 5

storage_limit = 1000

hardness_lower_bound = 3

hardness_upper_bound = 6

initial_storage_amount = 500

final_storage_amount = 500

maximum_vegetable_refinement_per_month = 200

maximum_non_vegetable_refinement_per_month = 250

if __name__ == "__main__":

# Create solver

solver = pywraplp.Solver.CreateSolver("GLOP")

# Index sets

I = range(0, prices.shape[1]) # oils

J = range(0, prices.shape[0]) # months

# Upper bounds

upper_bound_x = max(maximum_vegetable_refinement_per_month, maximum_non_vegetable_refinement_per_month)

upper_bound_b = storage_limit + upper_bound_x

upper_bound_y = maximum_vegetable_refinement_per_month + maximum_non_vegetable_refinement_per_month

# Define variables

x = [[solver.NumVar(0, upper_bound_x, f"x_{i}{j}") for j in J] for i in I] # amount of oil i to be refined in month j

b = [[solver.NumVar(0, upper_bound_b, f"b_{i}{j}") for j in J] for i in I] # amount of oil i to be bought in month j

s = [[solver.NumVar(0, storage_limit, f"s_{i}{j}") for j in J] for i in I] # amount of oil i in storage at the end of month j

y = [solver.NumVar(0, upper_bound_y, f"y_{j}") for j in J] # production in month j

print("Number of variables =", solver.NumVariables())

# At most 200 tons of vegetable oils refined per month

for j in J:

solver.Add(x[0][j] + x[1][j] <= maximum_vegetable_refinement_per_month)

# At most 250 tons of non-vegetable oils refined per month

for j in J:

solver.Add(x[2][j] + x[3][j] + x[4][j] <= maximum_non_vegetable_refinement_per_month)

# Amount of product produced in month j

for j in J:

solver.Add(sum(x[i][j] for i in I) == y[j])

# Hardness lower bound fulfilled

for j in J:

solver.Add(sum(hardness[i] * x[i][j] for i in I) >= hardness_lower_bound * y[j])

# Hardness upper bound fulfilled

for j in J:

solver.Add(sum(hardness[i] * x[i][j] for i in I) <= hardness_upper_bound * y[j])

# Exactly 500 of each type remaining at the end of june

for i in I:

solver.Add(s[i][5] == final_storage_amount)

# Storage at the end of a month is consistent with the initial storage, the amount bought and the amount refined

for i in I:

for j in J:

if j > 0:

solver.Add(s[i][j] == s[i][j-1] + b[i][j] - x[i][j])

# Storage at the end of January is consistent with initial storage of 500 of each type

for i in I:

solver.Add(s[i][0] == initial_storage_amount + b[i][0] - x[i][0])

# Objective function

material_costs = sum(prices.iloc[j].iloc[i] * b[i][j] for i in I for j in J)

storage_costs = storage_cost_per_ton_per_month * sum(s[i][j] for i in I for j in J)

revenues = price_per_ton * sum(y[j] for j in J)

objective = revenues - material_costs - storage_costs

solver.Maximize(objective)

# Solve the program

status = solver.Solve()

# Check if a solution was found

if status == pywraplp.Solver.OPTIMAL:

print('Solution:')

print('Objective value =', solver.Objective().Value())

for i in I:

for j in J:

print(f'x_{i}{j} =', x[i][j].solution_value())

print(solver)

else:

print('The problem does not have an optimal solution.')

Number of variables = 96

Solution:

Objective value = 107842.59259259261

x_00 = 0.0

x_01 = 96.29629629629616

x_02 = 85.18518518518539

x_03 = 159.25925925925924

x_04 = 159.25925925925924

x_05 = 159.25925925925927

x_10 = 199.99999999999997

x_11 = 103.70370370370384

x_12 = 114.8148148148146

x_13 = 40.74074074074074

x_14 = 40.74074074074074

x_15 = 40.74074074074074

x_20 = 0.0

x_21 = 0.0

x_22 = 0.0

x_23 = 0.0

x_24 = 0.0

x_25 = 0.0

x_30 = 250.0

x_31 = 37.49999999999937

x_32 = 0.0

x_33 = 250.0

x_34 = 250.0

x_35 = 250.0

x_40 = 0.0

x_41 = 212.50000000000054

x_42 = 250.0

x_43 = 2.7755575615628914e-14

x_44 = 2.7755575615628914e-14

x_45 = 2.7755575615628914e-14

<ortools.linear_solver.pywraplp.Solver; proxy of <Swig Object of type 'operations_research::MPSolver *' at 0x7f53d90ae9a0> >